Table of content

One thing many financial experts frequently mention is the need to have an emergency fund. This essentially represents a certain amount of cash reserves which people can use in times of the financial emergency.

Now, there are some obvious questions a number of market participants have: Do traders and investors need to have emergency funds? Since those people already have some amount saved up is it better to invest all of those amounts? Or is it a better option to retain some of those amounts for the emergency fund?

Some people might think that since traders and investors already have some funds, they might be better off investing all of those amounts and potentially earn some returns in the process. After all, if they face some financial emergency in their lives, they always have an option to liquidate some of their positions and withdraw the necessary funds in order to pay for those emergencies.

This might sound like a logical argument. However, there are some problems with this line of reasoning. Firstly, it is worth mentioning that if the market participants do not have an emergency fund to speak of, then they might be forced to sell some of their positions during the bear market and consequently liquidate those positions at a loss. On the other hand, if they have some cash reserves to fall back on, then they can retain their positions and only close them when the market rates are more favorable.

The second important factor here to take into account is the psychological aspect of trading and investing. The fact of the matter is that those market participants who have emergency funds are more likely to maintain control over their emotions, then those people who are risking all of their cash reserves in daily trades.

Finally, it is important to point out that having a sizable emergency fund can represent a prudent insurance policy against the economic downturn. Those are usually the worst times to sell investments since during the 2008 Financial Crisis many stocks have lost half or three quarters of their value. Consequently, those people who have emergency funds have some sort of insurance policy against job loss or missing mortgage payments without having to pay any premiums.

Understanding Emergency Funds

Before moving on to the exact advantages or disadvantages of having cash reserves, it is important to define what is an emergency fund. Well, this name is usually used with cash reserves which an individual or an organization holds in case of emergency. Obviously one does not need to register some sort of fund in order to have an emergency fund.

Instead, this term can be applied to emergency savings accounts in a bank. Or alternatively, this can be a money market account. Some people also hold a certain amount of physical cash at home as well. All of those things can be characterized as an emergency fund.

The main principle here is that the funds should be available for use at all times, which is usually true for those categories we have discussed above. This means that those investments which involve locking up funds for a specific period of time might not represent the best examples of an emergency fund.

For example, in the case of the certificates of deposit, also known as CDs, the client invests a certain amount of money for a specific period of time, usually ranging from 3 months to 5 years. During this period in some cases, the customer might receive some interest payments from the bank, however one can not withdraw the principal amount without having to pay some hefty penalties. Therefore, CDs are not very liquid investments.

In addition to that, it is worth pointing out that the real estate investments can not be used as emergency funds either. The fact of the matter is that if for whatever reason an individual wants to access some liquidity from properties, he or she has to go through a rather lengthy process. An investor should put up the property for sale and wait for potential buyers. It goes without saying that in some cases this process might take months, instead of just a couple of days.

Obviously, one alternative to that is to take out the mortgage. However, it also has two distinct downsides. Firstly, most likely it will take some time for the mortgage application to be processed and approved. After all, one can not show up at the local branch and walk out in 5 minutes with the necessary cash at hand. The second issue here is that there are some considerable fees when it comes to those applications. Consequently, those fees can add up to a significant amount.

Therefore, the proper emergency fund should be available for withdrawal without any significant delays and therefore those funds should stay liquid.

The second important factor to consider here is that the emergency fund should only be used for emergencies. One should not tap into those funds just buy some new items at a local store or pay for a dinner at a restaurant.

Instead, it should be used for such emergencies as repairs for cars or appliances, or for purchasing food, hygiene products, and other essentials if one loses a job, as well as for medical expenses. In fact, some people also keep a certain amount of cash at hand, in case they can not get access to the ATMs in times of natural disaster or other emergencies.

The main idea here is that once the emergency is over and an individual receives some income, he or she should refill the fund, as not to deplete it.

Building an Emergency Fund

So we have already defined and explained the meaning of the emergency fund. However, at this stage, the next logical question is: how one can build an emergency fund? Well, one thing many financial experts point out very frequently is that it is recommended for beginners to start with small amounts of money. This is because it is unrealistic to expect an individual to save thousands of dollars at once when he or she has never done this before.

Psychologically speaking, saving small amounts of money is much easier to achieve and it can certainly help to build a habit in the process. The exact amount of money saved on a monthly or weekly basis depends on the individual’s income and expenditure levels. For example, some people might be quite comfortable with saving $100 a week, which can add up to $5,200 a year. At the same time, some people might choose other amounts as their goal. The most important thing is to save money regularly and maintain consistency at all times.

One thing people have to determine here is the overall size of an emergency fund. There are no standard universally accepted norms for this. Every financial expert and commentator has his or her own opinion about the subject. For example, Dave Ramsey recommends people to build a $1,000 emergency fund before tackling their debts and then after that maintain 3 to 6 months worth of expenses as cash reserves.

So as we can see the size of the emergency fund depends on several factors. The local prices of goods and services, the size of the family, and the age of family members all play a role in determining the appropriate amount for an emergency fund.

Once an individual determines the size of an emergency fund, it becomes much easier to manage the household finances. What an individual can do here is to fully fund the emergency fund and then move on the extra money to trading or investment accounts.

It is also important to point out that the size of the emergency fund has to be adjusted from time to time in order to reflect the changes in individual circumstances, as well as to take into account the inflation. One does not have to do this every month, but it might be appropriate to make those adjustments at least for an annual basis. After all, if an individual does not increase the size of the emergency fund, it will start losing its purchasing power and become less effective in dealing with emergencies.

Emergency Funds and Investing

At this point, there are some important questions to answer: why would an investor and a trader consider having an emergency fund? After all, some of those people have quite a sizable trading and investment accounts. Can they not just invest all of their savings in the market and withdraw funds from those accounts when they face some financial difficulties?

Well, they can do so, but this might lead to some problems. One thing to remember here is that when investors have no emergency funds to speak of, they have to liquidate some of their investments every time they face any financial difficulties. It might happen that those emergencies take place in times of bear markets. Consequently, in those cases, the individual will be forced to sell some of the investments at a loss. Over time those losses can add up to a significant amount.

At the same time, the investor might purchase a stock which is considerably undervalued and has a prospect of significant capital appreciation. However, in order for investors to make those gains, they have to hold those investments for some time. Yet, if they have to liquidate their investments it will become impossible for them to make those gains.

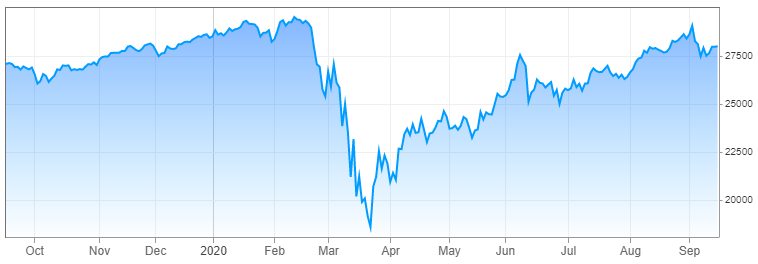

Let us take a look at a couple of examples of such a scenario, the chart below shows the Dow Jones Industrial Average for the last 12 months:

source: cnbc.com

As we can see from the above diagram, the index was in a solid upward trend during 2019, eventually reaching a peak near 29,500 by February 2020. This was followed by a sharp correction in March, with the Dow Jones Industrial Average fell all the way down to 18,600. This means that during such a short timeframe the index has lost approximately 37%, which is more than 1/3 of its value. So obviously, if an investor had Dow Jones Industrial Average stocks and was forced to sell stocks then the amount of losses would have been considerable.

Despite this major collapse, during the subsequent months, the index has recovered steadily, eventually returning to 28,000 level, erasing most of its recent losses in the process.

It goes without saying that the Dow Jones Industrial Average was not the only index which suffered from the March 2020 stock market crash. Here we can take a look at the chart which displays the performance of the FTSE 100 index:

source: cnbc.com

As we can see from the above image, the FTSE 100 index has reached a peak in January 2020, when it surpassed the 7,600 level. However, after this development, the index has fallen sharply, at one point even falling below the 5,000 mark. This means that during this period FTSE 100 has fallen by more than 34%, which represents more than 1/3 of its value. It is obvious that March 2020 was a very bad time to sell stocks.

Consequently, this type of approach of not having an emergency fund can have a very negative impact on the overall size of returns for investors. Therefore, it is a much better option for investors to have an emergency fund in place. In this case, those individuals will be able to address their financial emergencies without having to sell any part of their portfolio.

The basic principle of an emergency fund is quite simple. If an investor faces some financial challenges then he or she can use money from the emergency fund. However, once the personal financial situation is stabilized, then the market participant rebuilds the emergency fund and restores it to the previous levels. Once per year or with some other predefined frequency, the investor increases the size of the fund in order to reflect the changes of price levels due to inflation and other factors.

The emergency fund is even more important for long term Forex traders and stock investors. The reason for this is that strategies associated with those do usually require holding on to a position with an extended period of time. Consequently, the absence of an emergency fund can disrupt those strategies and can significantly worsen the financial results of trading and investing.

Here it is also worth mentioning that the emergency fund is also important for day trading. This is because the absence of cash reserves can lead to frequent closure of positions, which always increases the overall amount of money spent on broker commissions. This is very similar to the mistake of some people putting their emergency fund money in the certificates of deposit. The result in each case is that individuals have to pay some hefty fees in order to get access to their own savings.

Psychological Factors

Not having a proper emergency fund does not only present investors and traders with financial problems. There can be psychological factors at play here as well. The fact of the matter is that nearly all financial experts and professional traders and investors warn market participants not to make trading decisions based on emotions.

Now, what happens here is that those market participants who have no emergency fund in place tend to have a harder time controlling their emotions during trading. Some financial commentators explain this phenomenon in the following terms: if you invest your emergency fund to trading then you have a lot to lose for failed trades and therefore more likely to make decisions based on emotions.

This is not surprising, since people are keeping an emergency fund for paying for groceries, rent or mortgage, and other essential expenses in times of financial difficulty. So if market participants lose all of their money in trading, then they will have nothing to fall back on in case of financial setbacks or emergencies. Consequently, they are worried about the prospect of losing all of the money, and their decisions are influenced by their emotions.

On the other hand, when traders have their emergency fund in place, they are well-positioned to maintain control over their emotions. After all, they know that in the worst case scenario they will at least have enough funds to cover all of their essential expenses. Consequently, they are more likely to base their trading decisions on objective data, with fundamental and technical analysis, rather than their emotions.

In order to illustrate the significance of controlling emotions in trading and investing, let us take a look at his chart which shows the stock price performance of McDonald’s (MCD) for the last 5 years:

source: cnbc.com

As the above diagram shows, the McDonald’s stock had quite a strong showing during those years. Back in late 2015, the shares were trading near $98 level. During the subsequent years, the shares have risen steadily, before reaching an all time high of $217 during February 2020.

This was followed by a major correction in March. As a result of the stock market crash, MCD fell all the way down to $148. Now if that point investors panicked and decided to liquidate all of their McDonald’s investment, then most likely they would have ended up with a loss and eventually regret this decision.

The fact of the matter was that despite this major setback in March 2020, during the following months, the McDonald’s shares recovered and by September 2020, reached a new all time high of $225.

In addition to that having an emergency fund can certainly reduce the stress levels of traders. When traders risk all of their money down to the last penny on trades, this makes the entire experience of trading very stressful. Over time, this ‘all or nothing’ approach can take a toll on traders and interfere with their ability to make rational decisions. On the other hand, the fact that the market participants have something to hold on to can make their experience of trading much less stressful.

Free Insurance Policy Against Economic Downturn

When discussing the benefits of having an emergency fund for traders, it is worth mentioning that it also represents a type of insurance policy against the economic downturn. The fact of the matter is that when economic conditions worsen many people tend to lose their jobs, including those who trade Forex or Stocks on a daily basis.

Consequently, this makes it more difficult for those people to cover the basic expenses such as groceries, rent, and mortgage payments. Now, depending on the location of an individual some insurance companies offer people an opportunity to ensure their credit payments against unemployment.

However, obviously, the insurance companies are not charitable organizations. They need to earn some income and profits in order to cover their operating expenses such as salaries, rents, the cost of utilities as well as equipment. In addition to that, they also have to deliver dividends or share buybacks to shareholders. Consequently, those firms design their insurance premiums in a way to spend less money on insurance claims, compared to the revenues, which allows them to make a profit.

Generally speaking, an insurance premium represents a certain percentage of the total value of the potential payout. For example, let us suppose that an individual takes out an unemployment insurance plan, which pays $30,000 in the event of job loss. In this case, if the annual premium payments are 5% of this total amount, then an individual has to pay approximately $125 on a monthly basis. This means that the total annual amount of premium payments will be the equivalent of $1,500.

It goes without saying that one can not bypass such things as car or health insurance, for some obvious reasons. However, when it comes to the unemployment or bank credit default insurance one can supplant it with an emergency fund.

This is because the emergency fund fulfills exactly the same function as those two types of insurance products, however, it does have certain advantages over those as well. Firstly, people do not have to worry about filing the insurance claims and then about whether or not those claims will be accepted by those firms. In the case of an emergency fund, it is always at their disposal, regardless of the personal financial circumstances.

Another advantage of having an emergency fund over choosing those two insurance products is that it is free of charge. With an emergency fund, the individual does not have to spend hundreds of dollars on insurance premiums on a monthly basis. In fact, traders and other individuals are able to retain all of their savings and only use them in times of an emergency.

Credit Cards vs Emergency Fund

Despite those benefits of having an emergency fund, some financial experts, as well as some experienced traders might argue that credit cards might represent a viable alternative.

The argument here goes as follows: instead of traders and investors accumulating thousands of dollars in the bank savings accounts, earning a near-zero interest rate, would it not be better for them to invest those amounts in the market? In this way, they will have the ability to earn some decent returns on their capital. As for the possible emergencies, the market participants can simply use their credit cards to cover those unexpected expenses. In this way, investors do not have to liquidate their positions at a loss.

At one glance this method seems to address some of the downsides of not having an emergency fund. However, despite those upsides, the use of credit cards for this purpose does have a number of important disadvantages, something we will discuss below in a greater detail.

Firstly, it is important to recognize that unlike with the emergency fund, people do borrow money from the bank when they use their credit cards. Now, generally speaking, the bank mortgages usually carry the lowest interest rates, compared to other loan products. This is because the mortgage represents a type of secured loan, guaranteed by an actual asset, the property. So if the client fails to make necessary repayments, the bank has the ability to sell a home or other types of property to recover those funds.

Car loans typically have slightly higher interest rates than mortgages. This is because a vehicle represents a depreciating asset. However, even in this case, the bank has something to sell if the client defaults on his or her debts.

Now the situation with the consumer loans and credit cards is completely different. Those types of loans are unsecured. Obviously, the loan officer will look at the past credit history and current credit score of the bank’s clients before giving them credit cards and approving credit card limits. However, there is no collateral involved in this type of operation.

This means that if for whatever reason the client decides to default on the debt, the bank can not sell the collateral in order to recover those funds. Obviously, the bank management might decide to go to court in order for this purpose. However, even if they succeed in those attempts, in the best case scenario they might only recover some fraction of the entire balance. In the majority of cases, the credit card debt claims are settled by 10 to 50 cents per dollar, depending on the age of the loan as well as some other factors.

In addition to that, it is worth noting that banks usually go to court if the credit card balance is high enough for it to justify all of the expenses those institutions have to cover in order to sue their client and recover the funds. Consequently, banks and credit card companies typically do not go to court if the size of the balance is relatively small.

After all, paying thousands of dollars in court expenses just to recover a $300 credit card balance is counterproductive. The firm will just end up paying more money for those legal expenses, compared to the received amount. It is also worth noting that the company might be unable to recover any funds because the client might have no assets to speak of.

In order to compensate for those risks faced by financial institutions, they tend to charge higher interest rates on credit cards. For example, at current interest rates in the US, one can get a mortgage with an annual interest rate of 3% to 5%. On the other hand, when it comes to the credit card interest rates, they can go as high as 15% to 20%, depending on the credit rating of the borrower. This means that credit cards represent one of the most expensive loans one can have.

It is true that many banks have interest free repayment periods with credit cards. This means that if the client pays off the entire balance within 30 or 45 days, then the customer will not face any interest charges.

Now, the problem here is that the size of the financial emergency can be large enough to the extent that an individual might not be able to repay the balance before the end of this period. As a result, one will end up with a very high interest rate loan. Just to bring one example here, if a client holds $5,000 in credit card debt for 1 year, at 15%, then the total amount of interest will equal $750.

Finally, it is worth noting that there is no guarantee that the bank in question will always offer enough credit limit for the client to cover all of its financial emergencies. The fact of the matter is that according to the terms and conditions of using credit cards, the bank or credit card company has the ability to change interest rates or adjust the size of the credit limit at any point in time, without the consent of the client.

It is not surprising that in times of the economic downturn, many banks tend to reduce their exposure. One of the ways to achieve this is by lowering the credit card limit for clients. Therefore, when a financial emergency strikes, some people who are relying on credit cards might be left without any funds to deal with those problems. Consequently, it is much more reliable to have an emergency fund in place in order to cover any unexpected financial difficulties.

Emergency Fund for Investors and Traders – Key Takeaways

- An emergency fund is a term used to describe a cash reserve, which individuals and organizations have in place in order to tackle the unexpected financial emergencies. This can be in the form of a savings account, money market account, or even a physical cash. The exact recommended size of an emergency fund depends on one’s expenses, income, and other financial circumstances. Some financial experts also recommend increasing the size of the fund in line with inflation at least once per year, in order to maintain the purchasing power.

- Those market participants who have no emergency fund to speak of, have to liquidate some of their investments in order to deal with the unexpected financial problems. Consequently, sometimes they might be forced to close positions at a loss, which can significantly worsen their overall trading performance and reduce their earnings in the process. Therefore, traders and investors need an emergency fund to deal with their financial difficulties without having to liquidate their investments at the wrong time.

- Some people might suggest using a credit card instead of an emergency fund. This has at least two distinct disadvantages. Firstly, it is a well known fact that the interest rates on credit cards are much higher compared to other loan products. At the same time, it is worth keeping in mind that banks can always reduce the size of the credit limit, consequently, the funds might not be there one a trader might need it. Therefore having an emergency fund is a much more reliable option compared to credit cards.